|

17 Feb 2012

There was 44% growth in LED lighting market but the total market for LED components will be 'flat' for the next few years.

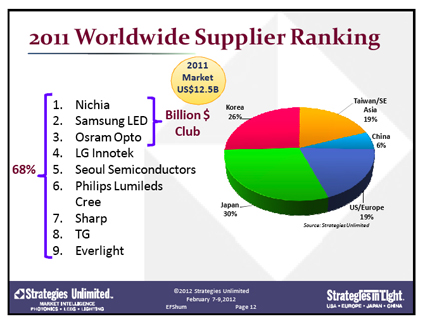

On the supply side, 10 companies accounted for almost 70% of the LED market. Strategies Unlimited arrived at these figures after analyzing market demand as well as the supply-side activity of more than 54 major LED component suppliers.

Top 10 suppliers in the LED market for 2011, by revenue of packaged LED components, were:

*Companies have the same ranking when the difference in revenue is within the margin of error. Revenue includes packaged LED sales only.

Geographically, Taiwanese and Chinese suppliers gained market share at the expense of the other regions. China's improvement in product quality, coupled with gains in the domestic market, fueled the growth from 2% market share to 6% in one year. Korean companies lost share in the slowing market, even though they were the most aggressive in increasing capacity during the ramp-up in 2010.

Philips Lumileds, Cree, and Osram Opto Semiconductors' expansion into 6-inch substrates slowed as there was a great deal of excess capacity in their existing 4-inch lines. The Japanese LED business has trended down or flat. However, Nichia and TG are major beneficiaries of the boom in tablet computers. Osram OS gained a major design win, which propelled its visible LED component business to more than $1 billion.

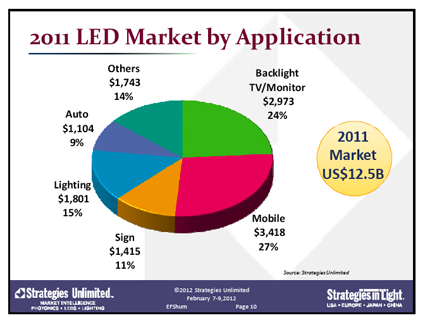

This segment stayed flat, at $3.4 billion. The overall decrease in the mobile phones market was offset by a sharp rise in tablet display and flash applications. A major development in this segment is the move to OLED displays. Approximately 50% of smartphone displays are expected to be OLEDs by 2016.

TV/Monitor Backlight

The LED revenue for TV and monitor backlights was $3 billion in 2011, but it is projected to drop substantially by 2016. The key disruptive factor in this segment is the introduction of low-cost direct backlit technology, targeted at sub-42-inch LCD TVs. This new technology can result in significant savings in the BOM, reducing the gap between LED and CCFL backlit TVs. These TVs are known as “Chubby TVs” since they are thicker than the slim edge-lit design the industry has been touting for the past few years.

The same supply conditions that reduced the price of LEDs increased the demand for packaged LED in lighting applications from $1.2 billion in 2010 to $1.8 billion in 2011. System efficacy, rather than LED efficacy, was the gating factor in 2011. The LED luminaire and replacement lamp market was $9.3 billion in 2011, an increase of 45% over 2010. The market for LEDs in lighting is expected to demonstrate substantial unit growth over the next five years, but revenue growth will be much lower due to pricing pressure.

Automotive

Revenue reached $1 billion in 2011 We expect a 5-year CAGR of 34% for LED headlamps. In addition to the styling issues, this is part of the trend to convert all front lighting to LEDs, as it will provide more front-end room for the car designer and reduce the overall system cost. Revenue for interior automotive lighting will show a modest decline over the next five years as instrument panel adoption reaches saturation and the market declines with prices.

Ella Shum's conclusions

The survey results were first presented by LED sector analyst Ella Shum at the annual Strategies in Light Conference between 7-9 February, in Santa Clara, California. In Shum’s keynote presentation – from which some of the main slides are presented here [right] – she made several notable observations and predictions:

“The LED count in devices is dropping fast and unit prices are dropping even faster. On the plus side she expects major growth in applications using low and mid power LEDs for solid state lighting although LED prices associated with these apps will drop the fastest.”

Advising LED developers on how they could increase profit margins Shum suggested the following actions: “Increase scale, efficiency and yield in manufacture; achieve premium pricing with application-specific packages; add value with embedded power management; invest in more R&D and testing to achieve higher operating temperatures, narrower binning and higher CRI; and strive for greater vertical integration.”

And Shum's key conclusions for the prospects of the industry in the coming year were: “The solid-state lighting market will take off; the overall market for LED components will be flat for next few years; and overall the industry should expect more consolidation and vertical integration.”

About the Author

Matthew Peach is a contributing editor to optics.org

|  |  |  |  |  |  |

| © 2026 SPIE Europe |

|