|

24 Aug 2005

Display glass is a big money-spinner for Corning, accounting for around a third of its revenue. James Tyrrell spoke with Pete Bocko, division vice-president and technical director of Corning Display Technologies, about the rise of its glass substrate business.

Corning Display Technologies is on a roll, having recently announced record second-quarter sales of $415 m (€335 m): a 30% increase over its first-quarter performance, and a 50% rise on the same period last year. In contrast, the firm's telecoms segment was down 3% on the first quarter, from $427 m to $415 m, and its optical fibre division slipped from a net income to a net loss following restructuring charges.

JT: It is tempting to say that Corning has been repositioning itself following the telecoms downturn, but is this really the case?

PB: Display has been a long time coming. It has been what we call "patient money" - people just didn't notice this activity because all of the focus was on telecoms.

The key event was really in the mid-1980s. We were doing a lot of experimentation with different glasses and different manufacturing platforms. This work was brought together in around 1984-1985 with the fusion process (see figure 1): a way of making exceptionally flat, clean and stable glass.

The platform that we built this on was developed originally for making eye-glass lenses. Believe it or not, they were actually going to punch them out like a cookie dough.

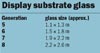

Critically, over time we've shown that the fusion process is extraordinarily capable of scaling up. Typically, when a new [size] generation comes out - Gen-5, Gen-6, Gen-7 (see box) - Corning has always been the first to commercialize a product.

How does your display glass differ from other glass products?

This is not ordinary window glass; it has very specific attributes. The glass has a high temperature capability, to suit the LCD manufacturing process, and no sodium contamination. We have made a huge investment in improving the melting and forming processes, and we're on our third-generation glass.

[According to the firm, its EAGLE2000 display glass, with a density of just 2.37 g/cm3, is the lightest LCD substrate glass on the market. The lower density improves handling during the display manufacturing processes, and switching from conventional 0.7 mm-thick substrates to 0.5 mm EAGLE2000 display glass is said to reduce weight by 35%.]

What are the challenges facing display substrate manufacturers?

Scaling up to the larger substrate sizes and maintaining quality are some of the big challenges. The television application is extraordinarily difficult as far as hitting LCD quality requirements goes. The other thing that I think all glass-makers are working on is manufacturing cost. In order for LCD television to meet its full potential, the expectation is that the cost of the glass has to go down. With LCDs, most of the cost is in the materials, not in the labour or the depreciation of the huge fabs.

How has substrate size changed to meet customer applications?

Gen-5 was targeted towards the computer monitor and driven by the ability to have very productive manufacturing for 17 or 19 inch displays. Everything after Gen-5 is about television. Gen-6 gives you a very efficient solution for 32 or 37 inch displays. As you get to Gen-7, you're talking 40 inches, and Gen-8, which we'll be delivering next year, is going to be 50 inches and above.

What do you see as the limit?

It is not necessarily the end application [or manufacturing] that is going to be the limit, rather the ability to ship the mother-glass around the country. The limits are things like tunnels and bridges. If we look at the soda-lime industry for architectural glasses - and we believe that it is going to be very similar with the LCD market - we might see something in the order of 3 × 3 m as being the ultimate large-size substrate. Transportation is going to be the driving factor.

Where are Corning's display customers located and how does this influence its manufacturing operation?

Customers are located in Japan, where the technology first emerged, Korea and Taiwan, and manufacturing is now starting in the Peoples' Republic of China. The glass has to be fresh, so you need to get it close to the customer. Also, it has been seen as a real strategic core of the LCD platform, so our customers insist that we locate our manufacturing capabilities in the countries in which it is required.

Does this present a challenge in terms of raw materials?

The sand has to have extraordinary quality requirements, but we have been able to locate sufficient raw materials in each of the locations. I think a bigger challenge for us right now is growing the organization.

We started by building an organization in Japan and then the next step was a joint venture with the Samsung group in Korea. We had a pre-existing joint venture for television [CRT], and so had access to some really top people, as well as to the market power of the Samsung group. Right now, we are putting a lot of effort into building a capable organization in Taiwan.

Looking to the future, do you think flexible displays are a threat?

No, I don't see them as a threat. The way these things roll out is not necessarily as a rapid disruption, but rather an evolution where people pull in new technologies. In time, we are going to see the back plane moving towards organic materials. I think that there are going to be certain niche applications that require a flexible display, but the all-organic display will probably require a glass-based solution.

Display technologies for mainstream applications take a long time to play out. People started working on plasma in the 1950s, and on active-matrix LCD in the 1960s. We are really looking to new applications to identify the disruptive technologies. |  |  |  |  |  |  |

| © 2026 SPIE Europe |

|